Retirement accounts often represent the largest marital assets after the family home. When a marriage ends, these accounts must be divided fairly—but unlike splitting a bank account, dividing pensions and 401(k)s requires specialized legal paperwork. A single mistake in this process can trigger tens of thousands of dollars in taxes, penalties, or permanently lost benefits.

The rules governing retirement division differ dramatically depending on account type. Some require court orders; others need only a letter from your attorney. Timing matters enormously: waiting too long can mean your ex-spouse withdraws funds, remarries and changes beneficiaries, or dies before you receive your share.

Understanding which accounts need formal court intervention, how the approval process works, and what tax consequences you'll face helps protect your financial future during an already difficult transition.

What Is a QDRO in Divorce?

A Qualified Domestic Relations Order (QDRO) is a court order that instructs a retirement plan administrator to pay a portion of one spouse's retirement benefits to the other spouse. Federal law—specifically the Employee Retirement Income Security Act (ERISA)—generally prohibits assigning or alienating pension benefits. The QDRO creates a narrow exception for divorce, allowing plan administrators to split accounts without violating federal rules.

The order must meet strict technical requirements. It identifies the "participant" (the employee who earned the benefits) and the "alternate payee" (the ex-spouse receiving a share). It specifies the exact dollar amount or percentage to be paid, which particular retirement plan is affected, and the number of payments or time period covered.

Not every retirement account requires this formal process. QDROs apply exclusively to employer-sponsored "qualified" retirement plans governed by ERISA. These include most 401(k)s, traditional pensions, 403(b) plans for nonprofit employees, and the federal Thrift Savings Plan. Plans must receive a properly drafted QDRO before they will divide assets—a divorce decree alone isn't sufficient.

Without a QDRO, the plan administrator will refuse to transfer funds to the non-employee spouse. The participant retains full control over the account, creating risk that assets will be spent, borrowed against, or otherwise diminished before the non-employee spouse receives their court-ordered share.

Which Retirement Assets Require a QDRO?

The requirement hinges on whether the plan is "qualified" under federal tax law. Qualified plans receive favorable tax treatment but must follow ERISA rules, including the QDRO requirement for division. Non-qualified accounts can be divided through other mechanisms.

Author: Natalie Brookstone;

Source: sbardellaorchards.com

401(k) and Pension Plans

Traditional employer pensions that pay monthly benefits for life always require a QDRO. These defined-benefit plans calculate payments based on salary history and years of service. The QDRO might award the alternate payee a percentage of the monthly benefit when the participant retires, or it might assign a lump sum representing the present value of future benefits.

401(k) plans, 403(b) plans, and similar defined-contribution accounts also fall under QDRO rules. These accounts have a current balance that can be divided immediately. The QDRO typically directs the plan to establish a separate account for the alternate payee or transfer a specified dollar amount directly to their own retirement account.

Profit-sharing plans, money purchase plans, and the federal Thrift Savings Plan all require QDROs. The key identifier: if your employer sponsored the plan and you received tax deductions for contributions, a QDRO is almost certainly necessary.

IRAs and SEP-IRAs

Individual Retirement Accounts operate under different rules. Because IRAs aren't employer-sponsored plans subject to ERISA, they don't require QDROs. Instead, the divorce decree or separation agreement directs the IRA custodian to transfer funds. The IRA owner completes a standard transfer form, and the custodian moves the specified amount to an IRA in the other spouse's name.

This "transfer incident to divorce" avoids taxes and penalties when executed properly. The transfer must occur directly between custodians—never withdraw funds yourself and hand them to your ex-spouse, as that triggers immediate taxation.

SEP-IRAs and SIMPLE IRAs follow the same rules as traditional IRAs. Despite being employer-established, they're technically individual accounts, so the simpler transfer process applies. Roth IRAs also use this method.

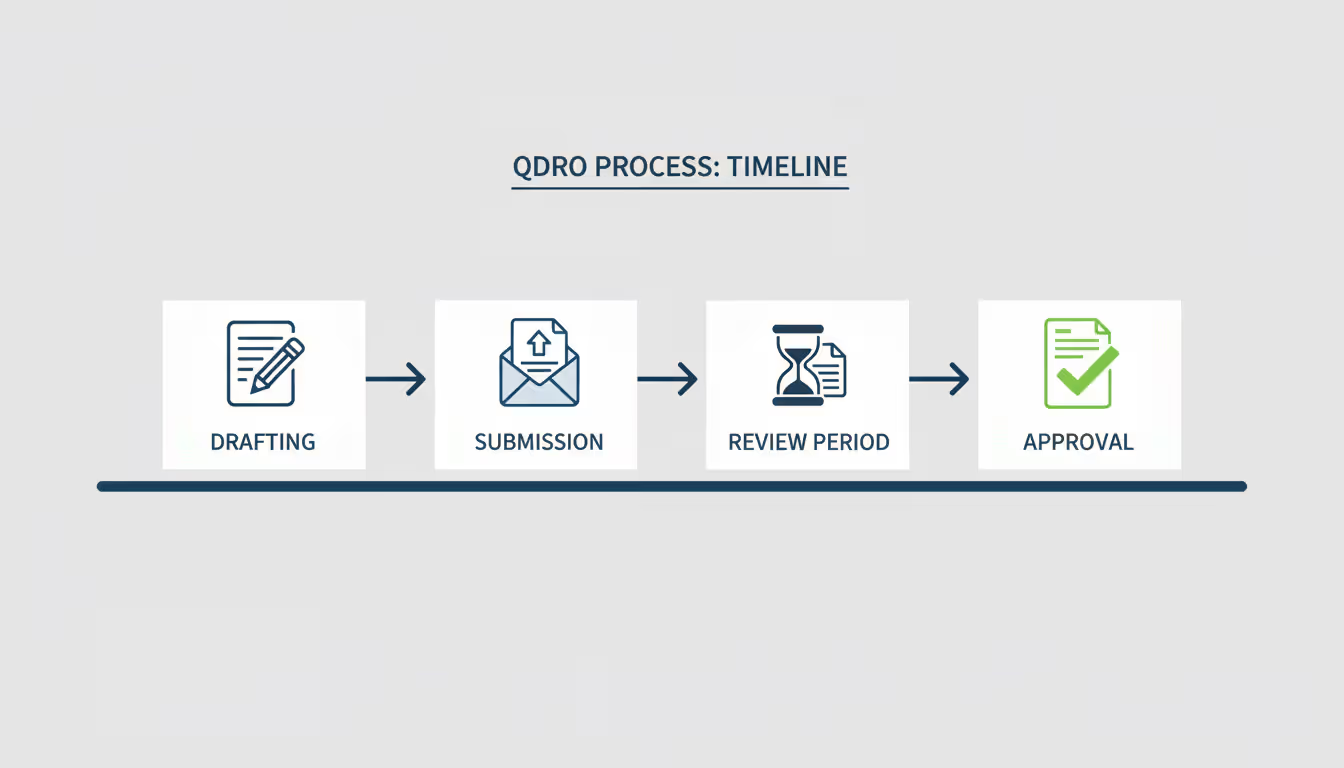

How to Divide Retirement Accounts in Divorce

The division process involves coordination between attorneys, the court, and plan administrators. Missing steps or cutting corners creates problems that can take years to resolve.

Step 1: Identify all retirement accounts. Both spouses should disclose every retirement account accumulated during the marriage, including old 401(k)s from previous employers. Request statements showing balances as of the separation date.

Step 2: Negotiate the division in your settlement. The divorce decree or marital settlement agreement must specify which accounts will be divided and what percentage or dollar amount each spouse receives. Vague language like "retirement accounts shall be divided equitably" creates problems later. Instead, use precise terms: "Wife shall receive 50% of the marital portion of Husband's Acme Corp 401(k) account, valued as of the date of separation."

Step 3: Obtain plan documents. Contact each plan administrator and request the Summary Plan Description and the plan's specific QDRO procedures. Many plans provide model QDRO language or pre-approved forms. Using the plan's preferred format dramatically speeds approval.

Step 4: Draft the QDRO. An attorney experienced in QDROs prepares the order based on your settlement terms and the plan's requirements. The document must include the participant's and alternate payee's full names and addresses, the plan name, the amount or percentage to be paid, and how payments will be made.

Step 5: Submit for plan pre-approval. Before presenting the QDRO to the judge, send a draft to the plan administrator for informal review. Administrators will flag problems that would cause rejection, allowing corrections before the order becomes official.

Step 6: Court approval. Once the plan administrator confirms the draft meets their requirements, submit it to the judge for signature. The court enters the QDRO as an official order.

Step 7: Formal submission to the plan. Send the court-signed QDRO to the plan administrator. They conduct a formal review (typically 30-90 days) and, if everything is proper, designate the alternate payee's account or begin payments.

Step 8: Choose distribution options. The alternate payee typically decides whether to keep funds in the plan (if allowed), roll them to their own IRA, or take a cash distribution. Rolling to an IRA preserves tax-deferred status; taking cash triggers ordinary income tax.

QDRO Timeline and Approval Process

From drafting to final approval, QDROs typically take three to six months. Simple 401(k) divisions with cooperative plan administrators might finish in eight weeks. Complex pension divisions involving survivor benefits can stretch beyond a year.

Several factors affect timing. Plans that provide model QDRO language and dedicated QDRO specialists process orders faster than small company plans that rarely handle divisions. Backlogs at the plan administrator's office create delays, particularly at year-end when many plans are busy with annual reporting.

Errors in the QDRO itself cause the most significant setbacks. If the order contains incorrect plan names, misstates the participant's employment dates, or requests benefits the plan doesn't offer, the administrator will reject it. The attorney must then redraft the order, obtain a new court signature, and resubmit—adding months to the timeline.

Plan administrators typically have 18 months to determine whether a domestic relations order qualifies as a QDRO, though most respond much faster. During the review period, the plan segregates the amount in question, preventing the participant from accessing those funds but not yet transferring them to the alternate payee.

Once approved, the plan establishes the alternate payee's rights. For defined-contribution plans, this usually means creating a separate account or processing a direct rollover within 30 days. For pensions, the alternate payee becomes entitled to their share of future monthly payments, though actual payments may not begin until the participant retires.

Delays carry real risks. If the participant retires, takes a loan against the 401(k), or dies before the QDRO is approved, the alternate payee may lose part or all of their intended share. Some plans allow loans or withdrawals even during the segregation period if the participant maintains sufficient vested balance.

Author: Natalie Brookstone;

Source: sbardellaorchards.com

Tax Implications of Dividing Retirement in Divorce

Retirement divisions create tax consequences that differ dramatically from other asset splits. Understanding these rules prevents expensive surprises.

When an alternate payee receives funds through a QDRO from a 401(k) or pension, those funds are taxable to the alternate payee, not the participant. This represents a significant shift: the person receiving the money pays the tax, even though the participant earned the benefits. If the alternate payee rolls the distribution directly into their own IRA or qualified plan, no immediate tax is due. The funds remain tax-deferred until withdrawn in retirement.

Taking a cash distribution triggers ordinary income tax at the alternate payee's current tax rate. However, QDRO distributions receive special treatment regarding the 10% early withdrawal penalty. If the alternate payee is under age 59½ and takes cash, they pay regular income tax but avoid the early withdrawal penalty that normally applies to pre-retirement distributions. This exception applies only to QDRO distributions, not to subsequent withdrawals from the alternate payee's own IRA after rolling funds over.

For IRA divisions, the tax treatment differs. A proper transfer incident to divorce creates no taxable event for either party. The receiving spouse takes over the IRA with the same tax characteristics it had before. A traditional IRA remains a traditional IRA; a Roth IRA remains a Roth. Future withdrawals are taxed according to normal IRA rules based on the new owner's age and circumstances.

Pension divisions involve additional complexity. If the QDRO awards the alternate payee a share of monthly payments beginning when the participant retires, each payment is taxable income to the alternate payee when received. The participant doesn't report that portion as income. If the alternate payee receives a lump sum representing the present value of future pension benefits, that lump sum is taxable unless rolled to an IRA.

Plans withhold 20% for federal taxes on direct cash distributions to the alternate payee unless the funds go directly to an IRA or qualified plan. State withholding may also apply. The alternate payee can adjust withholding by filing Form W-4P with the plan administrator.

Beneficiary Changes and Social Security Considerations

Author: Natalie Brookstone;

Source: sbardellaorchards.com

QDROs affect who receives benefits if the participant dies, but the interaction with beneficiary designations and Social Security requires careful attention.

Most retirement plans allow participants to designate beneficiaries who receive account balances or ongoing pension payments if the participant dies. A QDRO supersedes these designations for the portion awarded to the alternate payee. Even if the participant names their new spouse as beneficiary after the divorce, the ex-spouse with a QDRO receives their court-ordered share first.

For pensions offering survivor benefits, the QDRO can provide that the alternate payee continues receiving payments if the participant dies. This is called a "survivor annuity" provision. Without this language in the QDRO, the alternate payee's rights may terminate at the participant's death, even if they were still expecting years of payments. Attorneys must explicitly address survivor benefits in the QDRO if the alternate payee wants continued protection.

If the participant dies before the QDRO is finalized, the situation becomes complicated. Some courts have held that the alternate payee's rights vest upon entry of the divorce decree, even without a completed QDRO. Others require the QDRO to be in place before death. This uncertainty makes completing the QDRO promptly critical—don't wait months or years after the divorce to finish this paperwork.

Social Security benefits operate independently from QDROs. A divorced spouse may claim Social Security benefits based on their ex-spouse's earnings record if the marriage lasted at least 10 years, both parties are at least 62, and the claiming spouse is unmarried. These benefits don't reduce the ex-spouse's own Social Security payments. The QDRO dividing retirement accounts has no effect on Social Security divorce benefits—they're entirely separate systems under different laws.

However, some people confuse federal employee pensions with Social Security. The federal Thrift Savings Plan can be divided by QDRO, but federal Civil Service Retirement System (CSRS) or Federal Employees Retirement System (FERS) pensions require a different type of court order. These pensions can provide ex-spouse survivor benefits, but the rules differ from private-sector pensions.

The biggest mistake I see is couples who finalize their divorce without completing the QDRO, assuming they can handle it later. Six months go by, the participant changes jobs or retires, and suddenly the account they were supposed to divide is gone or substantially reduced. A QDRO isn't optional paperwork—it's the only mechanism that legally protects the non-employee spouse's share of retirement assets

— Jennifer Martinez

Common QDRO Mistakes to Avoid

Small errors in the QDRO process create disproportionately large problems. These mistakes appear repeatedly in divorce cases.

Waiting too long after the divorce. Some couples finalize their divorce and put off the QDRO, thinking they'll handle it eventually. Meanwhile, the participant retires and begins taking distributions, reducing the account balance. Or the participant dies, and the ex-spouse's claim becomes much harder to enforce. Draft and submit the QDRO while the divorce is pending or immediately after, not months or years later.

Using vague language in the divorce decree. Phrases like "retirement accounts shall be divided equally" don't provide enough detail for a QDRO. Specify the exact account name, the plan sponsor, and the precise percentage or dollar amount. If you're dividing the "marital portion" (the amount accumulated during marriage), define the start and end dates clearly.

Failing to address survivor benefits for pensions. If the pension participant dies before or during retirement, does the ex-spouse continue receiving payments? The QDRO must explicitly grant survivor benefits if you want that protection. Default plan rules often terminate payments at the participant's death unless the QDRO specifies otherwise.

Not obtaining plan-specific requirements. Each plan has its own QDRO procedures and model language. Using a generic form from the internet often leads to rejection. Always request the plan's QDRO guidelines and follow them precisely.

Author: Natalie Brookstone;

Source: sbardellaorchards.com

Ignoring loans or withdrawals during the divorce. If the participant takes a 401(k) loan or hardship withdrawal after separation but before the QDRO is entered, the account balance drops. Address this in your settlement—specify whether the alternate payee's share is calculated before or after such transactions, or prohibit the participant from accessing the account during the divorce.

Forgetting about old 401(k) accounts. People change jobs multiple times during a marriage. That 401(k) from an employer 10 years ago still exists unless it was rolled over or cashed out. Identify all retirement accounts, including old ones, and decide whether each will be divided.

Assuming IRAs need QDROs. Spending time and money drafting a QDRO for an IRA wastes resources. IRAs use a simple transfer process. Direct your attorney to use the correct procedure for each account type.

Retirement Account Division Requirements by Plan Type

Account Type

QDRO Required?

Division Method

Tax Treatment

Special Notes

401(k)

Yes

QDRO directs plan to split account or transfer funds

Alternate payee pays tax on distributions; no penalty if taken as QDRO distribution

Must use plan's specific QDRO procedures

Traditional Pension

Yes

QDRO awards share of monthly payments or lump sum

Alternate payee pays tax on payments received

Can include survivor benefit protection

IRA

No

Direct transfer incident to divorce via custodian

No tax if properly transferred; receiving spouse reports future withdrawals

Divorce decree directs transfer; no court order to plan needed

Roth IRA

No

Direct transfer incident to divorce via custodian

No tax on transfer; qualified withdrawals remain tax-free for receiving spouse

Maintains Roth character after transfer

403(b)

Yes

QDRO directs plan to split account or transfer funds

Same as 401(k): alternate payee pays tax unless rolled over

Common for teachers and nonprofit employees

TSP (Thrift Savings Plan)

Yes

QDRO using TSP-specific forms and procedures

Same as 401(k): alternate payee pays tax unless rolled over

Federal employees; TSP has strict QDRO requirements

Frequently Asked Questions

Do I need a QDRO for every retirement account in divorce?

No. QDROs are required only for employer-sponsored qualified plans like 401(k)s, pensions, and 403(b)s. IRAs, including SEP-IRAs and SIMPLE IRAs, don't need QDROs—they're divided through a direct transfer process using the divorce decree and custodian paperwork. Roth IRAs also use the transfer method. Check each account type individually, as mixing up the procedures causes delays.

How long does it take to get a QDRO approved?

Plan administrators typically review QDROs within 30 to 90 days after submission, though they legally have up to 18 months. The total timeline from drafting through final approval usually runs three to six months. Delays occur when the QDRO contains errors, the plan administrator has a backlog, or the plan has complex provisions. Using the plan's model QDRO language and obtaining informal pre-approval before court submission speeds the process significantly.

Will I pay taxes when I receive retirement funds through a QDRO?

You pay taxes only if you take a cash distribution. If you roll the funds directly from the plan into your own IRA or qualified retirement account, no immediate tax is due. The money remains tax-deferred until you withdraw it later. Cash distributions are taxed as ordinary income at your current tax rate, but QDRO distributions avoid the 10% early withdrawal penalty even if you're under 59½. Plan carefully with a tax advisor before choosing cash over a rollover.

Can a QDRO be changed after the divorce is final?

Modifying a QDRO after entry is difficult and often impossible. Courts generally allow corrections for clerical errors or to conform the QDRO to the original divorce settlement, but substantive changes require reopening the divorce case. If circumstances change—such as the participant switching jobs or the plan changing its structure—you may need a new or amended QDRO. This is why getting it right the first time matters so much. Don't rush the drafting process.

What happens if my ex-spouse dies before the QDRO is completed?

This creates a complicated legal situation. Some courts have ruled that the non-employee spouse's rights vest when the divorce decree is entered, even without a completed QDRO, meaning the estate can pursue the claim. Other jurisdictions require the QDRO to be in place before death for the non-employee spouse to have enforceable rights. Plan beneficiary designations may also come into play. This risk makes completing the QDRO immediately after divorce critical—don't delay.

Does a QDRO affect my Social Security benefits?

No. QDROs divide employer-sponsored retirement plans but have no impact on Social Security benefits. Social Security divorce benefits operate under completely separate rules. If your marriage lasted at least 10 years, you may claim Social Security based on your ex-spouse's earnings record without affecting their benefits. This right exists regardless of whether you received any portion of their 401(k) or pension through a QDRO. The two systems don't interact.

Dividing retirement accounts ranks among the most consequential financial decisions in divorce. These assets represent decades of work and future security. The technical requirements for QDROs, combined with the different rules for various account types, create opportunities for costly mistakes.

Start the QDRO process early. Don't wait until after the divorce is final to begin drafting. Work with attorneys who regularly handle retirement divisions and understand the specific requirements of different plan types. Obtain each plan's QDRO procedures and follow them precisely.

Remember that timing matters enormously. The longer you wait after divorce to complete a QDRO, the greater the risk that accounts will be depleted, the participant will retire or die, or plan changes will complicate the division. Treat the QDRO as an essential component of the divorce itself, not as optional follow-up paperwork.

For IRAs, use the simpler transfer process rather than attempting a QDRO. For 401(k)s and pensions, invest the time and money to get the QDRO right the first time. Consider working with a Certified Divorce Financial Analyst who can model the long-term impact of different division scenarios and help you understand the tax implications of various distribution options.

Your retirement security depends on properly executed paperwork completed promptly. The complexity of the rules means professional guidance isn't optional—it's essential protection for your financial future.

A prenuptial agreement is a legal contract signed before marriage that clarifies financial expectations and protects individual interests. This guide explains what prenups cover, why couples get them, how they're created, and answers common questions in plain language

Dividing retirement assets during divorce involves more than simply splitting an account balance in half. For most employer-sponsored retirement plans, you need a specialized court order called a Qualified Domestic Relations Order—commonly known as a QDRO

Prenuptial and postnuptial agreements define financial rights during marriage and divorce. Learn the differences between postnup vs prenup, legal requirements, enforceability factors, typical costs, and when these marital agreements make sense for your situation

A prenuptial agreement serves as a legally binding contract between two people planning to marry, establishing how assets, debts, and financial responsibilities will be handled during the marriage and in the event of divorce or death. This comprehensive guide explains everything couples need to know

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to family law, divorce, custody, child support, and related legal matters.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Legal processes may vary depending on jurisdiction, personal circumstances, and applicable laws.

This website does not provide legal advice, and the information presented should not be used as a substitute for consultation with qualified family law attorneys or legal professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.